Participation Models of Distributed Energy Resources

A Brief Look Into Future Energy Markets

A more dynamical distribution networks ~ The ability of end-users to bi-directionally transact energy and money with the utility company has introduced tremendous changes to the electricity distribution network, bringing considerable opportunities to the grid, including customer bill savings and back up services, energy mix diversification and decarbonization, and reliability and resiliency support. The bi-directionality also introduced multiple challenges to the conventional utility tariff model and to grid operators in the form of improper cost recovery and reverse power flows.

Distributed energy resources (DER), such as rooftop solar, batteries and flexible loads can provide, under proper participation schemes, customer services (e.g., bill savings), grid services (e.g., transformer upgrade deferral) and wholesale market services. The landmark ruling of Federal Energy Regulatory Commission’s (FERC) order 2222, aims to remove “the barriers preventing DER from competing on a level playing field in the organized capacity, energy and ancillary services markets run by regional grid operators”.

In this article we discuss three primary existing and futuristic DER participation models into both the retail and wholesale electricity markets:

· Model 1: Participation via a DER Aggregator (DERA)

· Model 2: Participation via a Distribution System Operator (DSO)

· Model 3: Participation via Peer to Peer (P2P)

Model 1: Participation via a DER Aggregator (DERA)

In this model, the DER Aggregator acts as an intermediary between the wholesale market and prosumers (end-consumers who sell back to the grid). It is worth noting that Independent System Operators (ISOs) do not have oversight over the distribution lines where prosumers are connected to the grid. This hinders direct interactions between ISOs and prosumers, and hence, the presence of the intermediary (DER Aggregator) becomes inevitable. However, when DERA is profit-seeking, wholesale and retail market designs need to be revisited, and perhaps, jointly analyzed. DERA now acts as a supplier in the wholesale market, while taking care of prosumer interaction. At the same time, DERA purchases energy from prosumers. One possible approach to capture such complex interactions is via game-theoretic techniques (see here).

Given that prosumer individual participation in the wholesale market is not operationally and economically feasible, DER Aggregator acts as an intermediary between the wholesale market and prosumers.

In a perfect world, prosumers would directly interact with ISOs and sell back to the grid at wholesale market prices, maximizing the market efficiency. However, this is far from reality. In the presence of DERA, with one-part pricing, DERA must buy energy from prosumers at a lower price to benefit from price arbitrage, and hence there must be a positive market efficiency loss. Interestingly, it has been shown that with two-part pricing, market efficiency can be fully preserved; DERA can still make profits by buying energy from prosumers at the wholesale price but needs to receive a fixed “connection charge” from prosumers.

An ongoing problem with model 1 is how can the DERA create enough incentive for individually rational customers to forego the lucrative utility retail program, e.g., Net Energy Metering (NEM), and enroll with DERA to provide grid and wholesale market services. A first attempt to solve this problem is offered here, where a DERA promises its customers a surplus that is higher than its benchmark — i.e., under the utility’s regime.

Model 2: Participation via a Distribution System Operator (DSO)

A renowned model for enabling DER to participate in providing distribution grid and wholesale market services is through a distribution system operator who emulates the wholesale electricity market (WEM) market clearing and pricing mechanisms. The DSO market-based model is motivated by the fact that retail prices are usually flat; not reflecting the dynamically varying cost of serving end-users which creates market inefficiencies, inequities and utility revenue shortfalls. For participation of DER under model 2, a distribution-level market is established, allowing the DSO to receive bids from the various market participants and makes financial settlements correspondingly.

The DSO is a price-taker in the wholelsale market and a price maker in its own local distribution market. synonymous to locational marginal prices (LMPs) in WEM, the DSO-operated market solves for the so-called distribution locational marginal price (DLMP) that optimizes a certain objective (such as social welfare or network congestion), while efficiently accounting for front-of-the-meter (FTM) and behind-the-meter (BTM) resources in the market such as solar farms and electric vehicles (see here). The LMP is determined by clearing transmission markets, which is then used by the DSO to clear local market to determine DLMP.

Under the local DSO market, DERA are also considered price-takers. They submit demands and bids to DSO, which then solves a program to maximize the benefits in the network using a forecast of the LMP to represent the marginal cost of delivering power to distribution network customers. The market clearing price the DERA faces at a certain bus is the DLMP solved for at the same corresponding bus.

A local DSO-based market could unlock the potential of DER, but it still lacks the proper interpretation of what DLMP represent and how voltage constraints, network congestions and losses affect it.

A similar, though smaller scale, model is the notion of energy community (e.g. community solar or microgrid), where the community operator accommodates its customers and aggregate their resources via two common paradigms:

i) An energy community, where the community operator takes the utility price, and makes the community price, which will be paid by the community members. Based on the price, the community customers determine their demand and BTM resources’ schedules.

ii) A centralized market structure where the community operator takes control of the customers’ demand and resources to achieve a predefined objective.

Although, model (ii) usually achieves higher optimality, it requires customers to drop their privacy and submit their resources information and consumption patterns to the operator. Additionally model (ii) may suffer computational complexities. Model (i) is more reasonable, but requires a careful design of pricing mechanisms that induce market efficiency and ensure fairness to all customers.

Model 3: Participation via Peer to Peer (P2P)

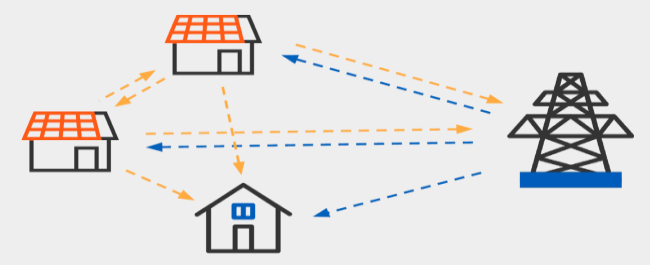

The P2P model’s key difference from models 1 and 2 is that it enables prosumers to exchange energy with other peer prosumers; turning them from price-takers to price-makers. Therefore, through bilateral contracts the peers can agree on the purchased quantity and price.

Multiple emerging technologies enabled the realization of P2P market structure, including marketplace and trading platforms and blockchains. A list of existing P2P projects can be found here and here. Researchers showed that P2P is able to achieve a more socially optimal solution in the distribution network (see here). The optimality of P2P hinges on designing a transparent and equitable mechanism that adequately incentivizes all customers to collaborate for the sake of achieving the socially optimal goal.

The challenge in the realization of P2P is the need for highly interdisciplinary backgrounds that can tap into prosumer psychology, rationality, and system modeling. Moreover, researchers need to back-project the P2P network into the greater picture of dynamically co-existing with other customers, utility companies, DSOs and ISOs.

The distribution grid is witnessing a considerable proliferation in the number of deployed DER, resulting in a more open and decentralized grid. The non-dispatchability of most DERs requires a careful look into their participation models and how to effecintly price their provided services. The phase-out of the generous 1:1 NEM retail programs to successors with lower compensation rates and solar-capacity-based fixed charges, increased DER systems’ payback times, which directly affected their economic feasibility. This gave rise to alternative DER participation models, which we discussed in this brief. The three discuussed participation models are: 1) participation via a DERA, 2) participation in a DSO-operated market, and 3) participation via P2P transactions. It is unknown which model is going to most properly accommodate the rising level of DER, but surely that model has to be efficient, transparent, just, and resonable in adequately incentivizes all customers and other entities to collaborate to achieve a socially optimal and reliable operational state.